ai reshaping insurance who benefits left behind 2026

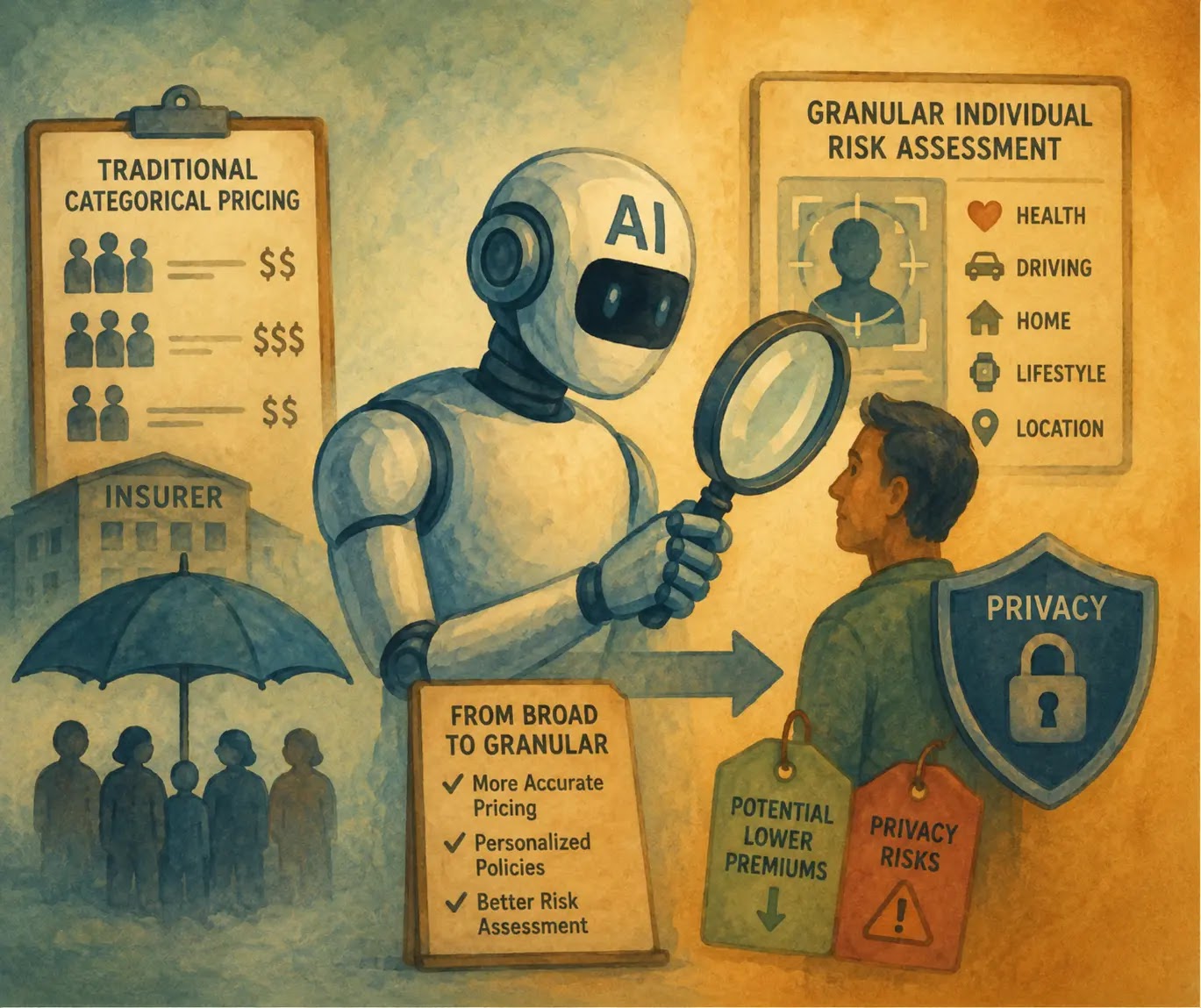

AI is transforming insurance from broad categorical pricing to granular individual risk assessment, with significant consequences for both premiums and privacy.

By Stuart Kerr, Technology Correspondent, LiveAIWire

The Way Your Insurance Premium Is Calculated Is Being Rebuilt From Scratch. Here Is What That Means for You.

Insurance is one of the oldest financial products in human history, and for most of its existence it has operated on the same fundamental principle: group people into broad risk categories based on a handful of observable characteristics, calculate the average expected loss for each category, and charge a premium that covers that loss plus a profit margin. Your car insurance premium has been determined largely by your age, your postcode, the make of your car, and your claims history. Your health insurance by your age and whether you smoke. Your home insurance by your property type and neighbourhood. These broad categories are efficient for insurers and deeply unfair to individuals whose actual risk profile is substantially better than the average for their category.

Artificial intelligence is dismantling that system and replacing it with something both more precise and more complex, with consequences for consumers that can be beneficial or harmful depending on where you stand in the risk distribution. The AI in insurance market is projected to grow from $26.3 billion in 2026 to $114.52 billion by 2031, a compound annual growth rate of 34.2 percent. Insurers using AI-powered analytics have generated 6.1 times the total shareholder return of those that have not over the past five years. The transformation is already underway at scale. Understanding what it means for you personally is now a practical necessity.

How AI Is Transforming the Quote You Receive

The most visible change for consumers is in the speed and personalisation of insurance pricing. Hiscox, the specialty insurer, achieved a 99.4 percent reduction in quote cycle time for London Market specialty lines, compressing turnaround from three days to approximately three minutes using agentic AI underwriting systems. For standard personal lines, AI-powered straight-through processing rates have jumped from 10 to 15 percent of applications to 70 to 90 percent, meaning the overwhelming majority of straightforward insurance applications are now assessed and priced entirely by AI without any human underwriter involvement.

The data feeding those assessments has expanded dramatically beyond the traditional handful of rating factors. AI insurance pricing models now incorporate medical records for health and life policies, property valuations and satellite imagery for home policies, real-time telematics data from connected vehicles for motor policies, IoT sensor data from smart home devices for property policies, and credit and transaction behaviour patterns across multiple lines. What used to take weeks of manual assessment now happens in moments, with AI models identifying risk signals that were previously invisible to human underwriters.

The practical result for many consumers is more accurate pricing that better reflects their actual behaviour and risk rather than the average for their demographic group. A careful driver with a clean record who drives relatively few miles pays less under telematics-based pricing than under a flat category model. A non-smoker with healthy lifestyle indicators can receive health insurance terms that reflect their genuine risk rather than being grouped with their age cohort. The movement from static, annual underwriting to continuous underwriting, where risk is assessed in real time based on streaming data from connected devices, represents the most fundamental shift in how insurance works in its long history.

The Claims Revolution: From Weeks to Hours

The impact of AI on claims processing is equally significant and arguably more immediately visible to policyholders. AI-powered claims automation is delivering 30 to 40 percent cost reductions per claim, with standard claims processing costs dropping from $40 to $60 to $25 to $36. Aviva, one of the UK’s largest insurers, is reporting more than $80 million in annual value from AI-driven claims optimisation. The Global Insurtech market is projected to reach $23.5 billion in 2026, with insurers using AI-powered claims automation resolving claims 75 percent faster.

For the policyholder, the practical experience of this shift is filing a claim through a smartphone app, receiving an AI-generated initial assessment within minutes rather than days, and in straightforward cases receiving a settlement decision without any human claims adjuster involvement at all. The AI analyses the evidence, cross-references it against policy terms, calculates the appropriate payment, and triggers disbursement automatically. Complex claims involving disputed liability, significant property damage, or potential fraud are escalated to human adjusters who focus their expertise where it is genuinely needed rather than spending it on routine cases.

The fraud detection dimension of AI claims processing is equally significant. AI-generated and manipulated images are appearing in claims across personal lines, commercial lines, and specialty coverages, from inflated home damage photographs to staged car accidents and synthetic medical scans. AI fraud detection systems are trained specifically to identify these manipulations, creating an arms race between AI-enabled fraud and AI-enabled fraud detection that mirrors the dynamic already visible in financial services.

The Winners: Those Whose Risk Is Better Than Average

The shift from broad categorical pricing to granular individual risk assessment creates clear winners: people whose actual behaviour and risk profile is substantially better than the average for their demographic group but who have historically been grouped with and priced like that average. Young drivers who drive carefully, infrequently, and in safe conditions can receive dramatically better telematics-based premiums than the age-group average would suggest. Healthy individuals whose lifestyle data demonstrates genuine low-risk behaviour can access health and life products priced for their actual profile. Small businesses with strong operational data and clean claims histories can receive commercial insurance terms that reflect their genuine risk rather than their industry category average.

For these policyholders, AI-driven insurance represents a genuine financial improvement. The precision of individual assessment replaces the bluntness of categorical averaging, and those who have been subsidising higher-risk members of their demographic group are the direct beneficiaries.

Who Gets Left Behind: The Risks That Deserve Honest Attention

The flip side of individual precision is equally important to understand. If AI pricing accurately reflects individual risk, the cost of insurance for genuinely higher-risk individuals rises. This has profound implications for groups including people with health conditions, drivers in high-crime areas, and homeowners in locations with elevated climate risk from flooding or subsidence. In a categorical pricing system, the cost of insuring high-risk individuals is subsidised by lower-risk members of the same category. In a precisely individualised system, that cross-subsidy disappears.

The regulatory concern that follows is significant. The EU AI Act classifies insurance underwriting and claims processing AI as high-risk systems, requiring rigorous documentation, human oversight, bias testing, and explainability. Colorado’s SB 21-169 requires insurers to demonstrate that their AI pricing models do not produce unfair discrimination. Grant Thornton’s 2026 AI Impact Survey found that 44 percent of insurance executives say governance or compliance challenges have contributed to AI projects failing or underperforming, and only 24 percent are very confident they could pass an independent AI governance review. The regulatory framework is tightening, but its enforcement remains uneven.

The data privacy dimension is equally significant. Telematics-based driving monitoring, smart home sensor data, wearable health monitoring, and lifestyle data gathered for insurance pricing represent a significant expansion of the information insurers hold about individual policyholders. As explored in The Invisible Algorithm Deciding Whether You Get a Loan, a Job, or a House, the principle that individuals should understand what data is being used to make consequential decisions about them, and should have the ability to challenge those decisions, is one that insurance regulators are only beginning to apply with appropriate rigour to AI-driven systems.

What You Should Do As a Consumer

Understanding the new insurance landscape requires a few practical adjustments to how you engage with the market. Telematics-based car insurance, where a device or app monitors your driving and prices your premium accordingly, is worth considering seriously if you drive carefully and infrequently. The premium savings for low-risk drivers can be substantial. Wearable health data sharing programmes offered by life and health insurers similarly offer financial benefits to individuals whose health metrics are strong, but warrant careful review of what data is shared, for how long, and under what conditions it can be used.

Shopping the market more frequently is increasingly worthwhile as AI-driven pricing means your optimal insurer may change as your circumstances and risk profile evolve. The aggregator and comparison site model is being enhanced by AI that can identify not just the cheapest premium but the most appropriate coverage structure for your specific situation. The question to ask any insurer offering data-sharing discounts is simple: what data are you using, how long do you retain it, and what happens to my premium if my circumstances change? A transparent answer to those questions is increasingly a reasonable expectation, and regulatory frameworks in both the EU and the US are moving to make it a legal requirement.

About the Author

Stuart Kerr is Technology Correspondent at LiveAIWire. He writes about artificial intelligence, ethics, and how technology is reshaping everyday life. Follow @LiveAIWire on X.