By

Stuart Kerr, Technology Correspondent,

LiveAIWire

Ninety-five per cent of UK insurance firms now use artificial

intelligence somewhere in their business, the highest adoption rate of any financial

sector, according to the Bank of England and Financial Conduct Authority’s

2024

survey of AI in UK financial services. That places insurers ahead

of banks and investment managers. It matters now because the same technology

deciding how fast your claim is paid is also deciding what you are charged,

and increasingly whether you can get cover at all.

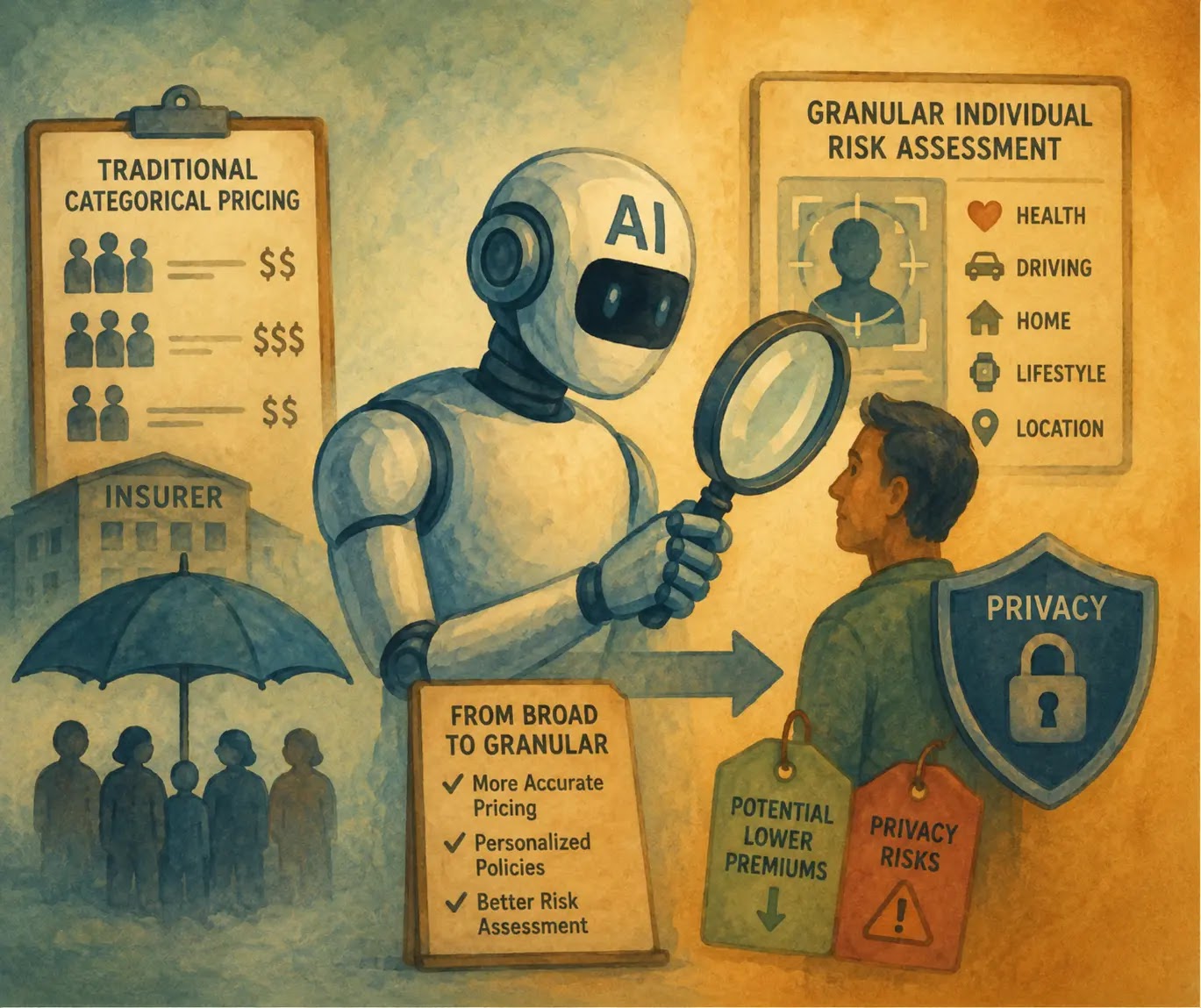

The Premium You Pay Is Now Set by a Machine

Pricing and underwriting, once the work of human actuaries poring

over tables, are now largely machine tasks. The European insurance regulator

EIOPA found that 50 per cent of non-life insurers and 24 per cent of life

insurers across Europe were already using AI across the value chain,

including pricing and underwriting, in its 2024

digitalisation review. The appeal for insurers is obvious. Models

trained on thousands of data points can price a risk in seconds and spot

patterns a person would never see.

For many customers that means faster quotes and, in low-risk

cases, lower premiums. A careful driver with a clean record and a telematics

box may pay less than they would have under a blunt human estimate. The

granularity cuts both ways, though, and the closer a model looks, the more it

can separate one customer from another.

Faster Claims Are the Industry’s Easiest Win

The clearest benefit shows up after something goes wrong. AI

systems now triage claims, read damage photographs, flag likely fraud and

settle simple cases without a human ever opening the file. EIOPA’s review

identified claims management and fraud detection as two of the most common

uses across European insurers, alongside pricing.

That speed is real and it favours the customer. A motor claim that

once took weeks can clear in days when software handles the routine paperwork

and routes only the awkward cases to a person. Fraud detection, meanwhile,

protects the honest majority, because every fraudulent payout is eventually

recovered through everyone else’s premiums. This is the part of the story

insurers are happy to tell, and on the evidence they are right

to.

The gains are easiest to see in motor and home cover. An insurer

using image recognition to assess a dented bumper from a few phone

photographs can issue a settlement before a human assessor would have booked

a visit, and that convenience is genuine. The same models that read those

photographs also scan for the tell-tale inconsistencies of a staged claim,

quietly screening out fraud that would otherwise be absorbed by every honest

customer through higher renewal prices. Where AI sticks to this work, sorting

the routine from the suspect, the case for it is strong and the customer

mostly benefits.

The People Algorithms Quietly Price Out

The harder story sits in who gets left behind. EIOPA warned in its

2024 review that AI driven pricing can lead to excessive standardisation and

a limited consideration of a customer’s specific circumstances. In plain

terms, a model optimised for the average can misread anyone who is not

average, and the people most often misread are those already on the

margins.

When a system prices on hundreds of correlated signals, it can

rebuild a picture of someone’s health, income or neighbourhood without ever

being told those things directly. The result can be higher premiums or quiet

exclusion for higher-risk and vulnerable customers, a concern EIOPA has

raised repeatedly as it presses supervisors to watch for unfair outcomes.

None of this requires malice. It is simply what happens when accuracy becomes

the only goal and fairness is left to look after itself. The same tension

surfaces in our coverage of AI

and the great insurance gamble, where finer prediction and fairer

treatment pull against each other.

The Black Box Problem Insurers Cannot Yet

Explain

Speed and accuracy come with a cost the industry is still

wrestling with: many insurers cannot fully explain how their own systems

reach a decision. The Bank of England and FCA survey found that a large share

of firms hold only a partial understanding of the AI they deploy, and that

foundation models, the complex systems behind generative AI, already account

for around 17 per cent of all AI use cases in UK financial services. When a

model is opaque even to the company running it, a customer trying to contest

a price or a refusal faces a steeper climb still.

This is why supervisors keep returning to transparency. A premium

you cannot interrogate is a premium you cannot challenge, and an insurer that

cannot show its working cannot easily prove it treated you fairly. The same

survey recorded that firms themselves see cybersecurity as the single

greatest risk attached to their AI, a reminder that the systems now holding

your most sensitive financial and medical data are also a target for the

people who would steal it. The more of the insurance relationship that

disappears into these models, the more the question of who can actually see

inside them comes to matter.

What This Means for You

For an ordinary policyholder, three practical habits now matter

more than they used to. Shop around harder, because two insurers running

different models can return startlingly different prices for the identical

risk, and loyalty is rarely rewarded. Ask what data a quote is based on,

since under UK data protection law you are entitled to know, and you can

challenge a decision made solely by automated means. And read the detail on

telematics or app-based policies before signing, because the discount on

offer is paid for with a continuous stream of data about how you drive, live

and move.

Consider a self-employed courier refused affordable motor cover

because a model reads gig-economy mileage as elevated risk. The fix is rarely

to argue with the algorithm. It is to find an insurer whose model weighs that

profile differently, which is why comparison and a willingness to switch are

now a consumer’s strongest tools. The wider shift from human to automated

decision-making across daily life runs through our look at the

automation divide.

The Next Five Years Will Decide Who Insurance

Serves

Regulators are no longer watching from the sidelines. Under the EU

AI Act, AI systems used for risk assessment and pricing in life and health

insurance are now classed as high-risk and face stricter requirements, and

EIOPA has issued guidance pushing insurers toward transparency and

accountability. Britain’s Bank of England and FCA are running their own

monitoring through repeated surveys and a dedicated AI consortium. The

question for the rest of this decade is whether that oversight keeps pace

with the models, or trails a step behind them. The technology that makes

insurance faster and cheaper for most people is the same technology that can

shut the door on a minority, and which of those outcomes wins will be settled

less by code than by the rules we choose to write around it. Britain has so

far favoured monitoring over hard legislation, leaving its regulators to lean

on surveys and supervisory pressure rather than statute, while Europe has

reached for binding law. Which approach better protects the customer who

finds themselves on the wrong side of a model is a question the next few

years will answer in public. For the deeper mechanics of how insurers turn

data into prices, see our guide to AI

in insurance, premiums and predictions.

About the Author

Stuart Kerr is Technology Correspondent at LiveAIWire, covering

artificial intelligence, cybersecurity, and the social impact of emerging

technology. He publishes daily at LiveAIWire.com.